Image

With deals in every state, Washington, D.C., and Puerto Rico, we’ll put 44 years of experience to work for you.

| Investment Experience | Social Impact |

|---|---|

|

|

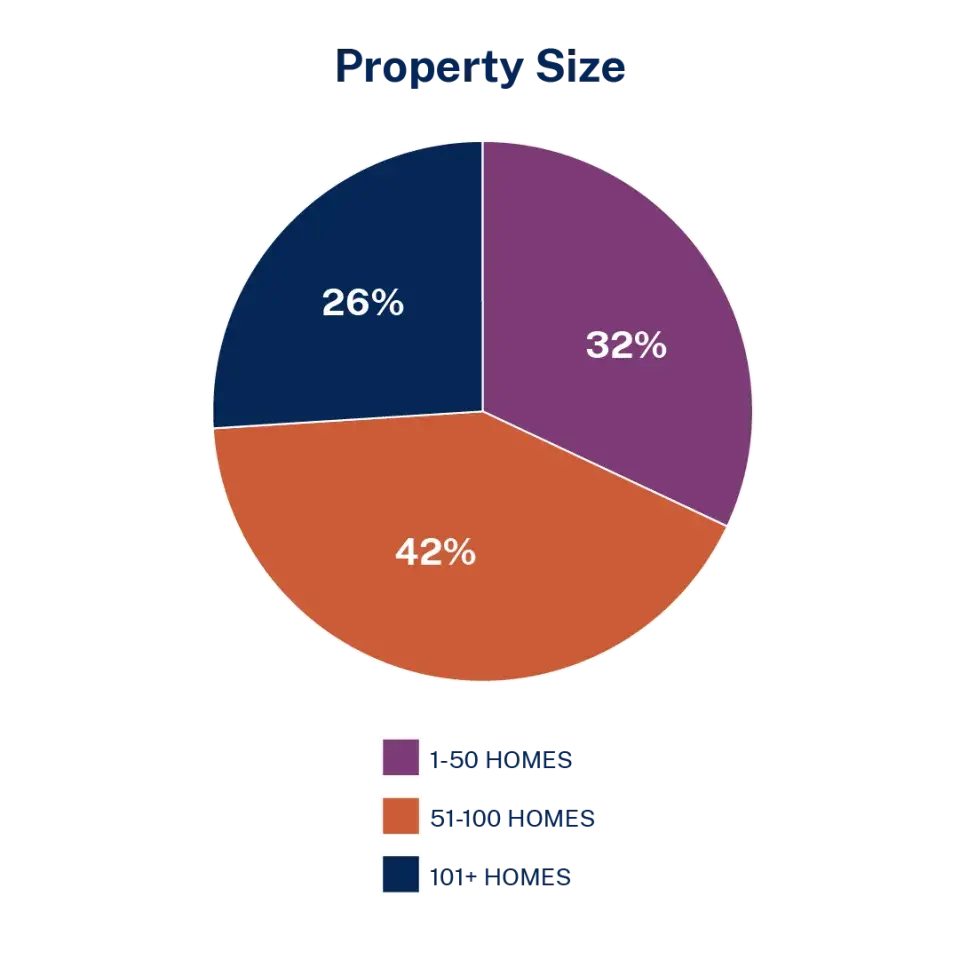

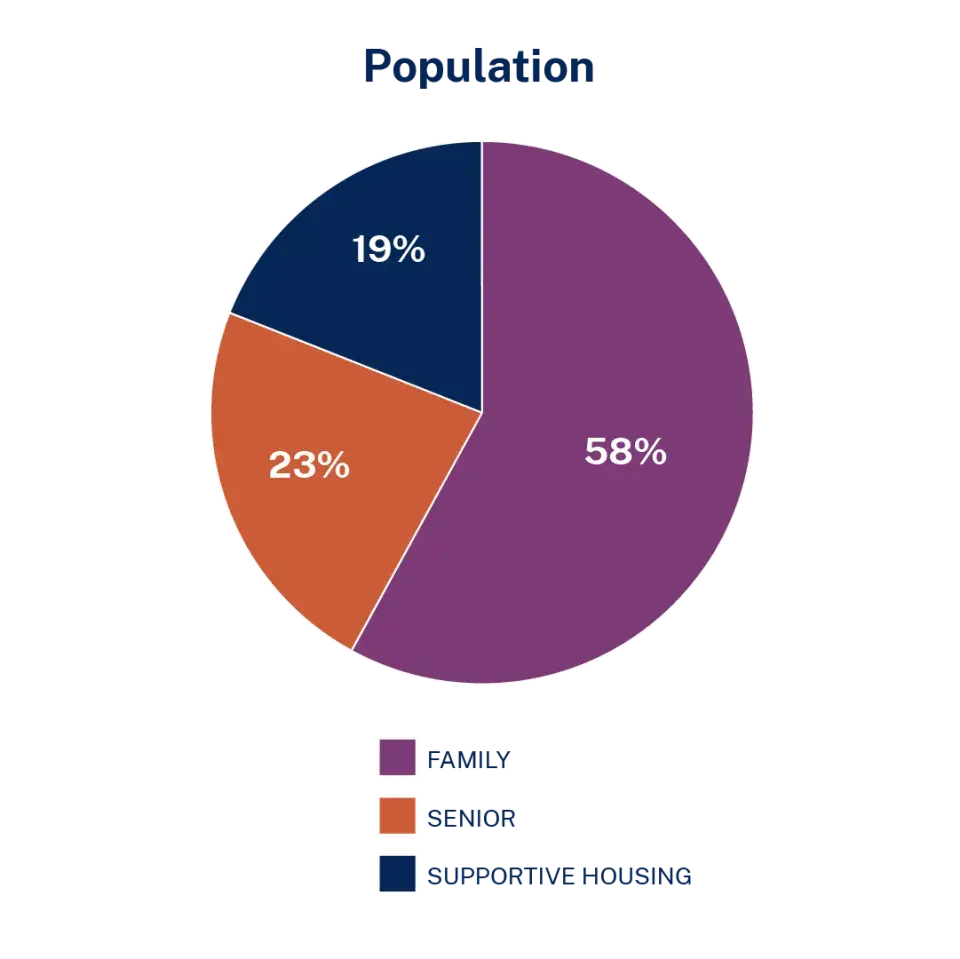

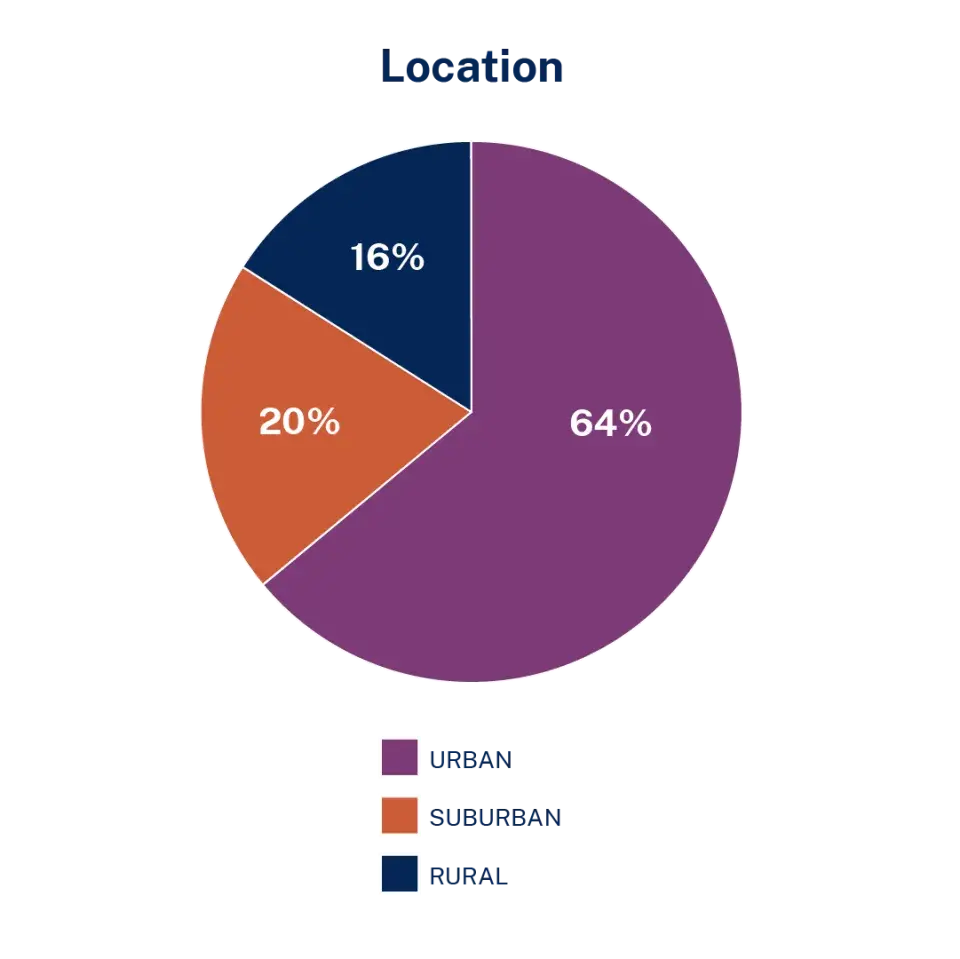

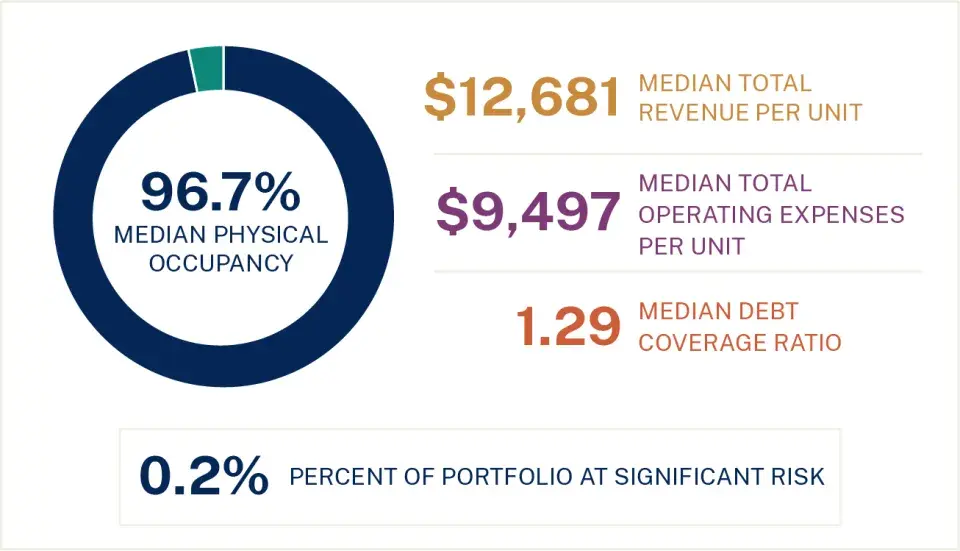

We manage over 1,305 properties in our current portfolio (net of dispositions). That represents 216,000 homes and $24.4 billion in invested equity.

Our annual Trends Analysis report gives the latest stats on our portfolio and strength.

|

Image

|

Image

|

Image

|

We’re an active listener and a proactive partner. First, we get to know you and your goals so we can recommend the best financial structure for your deal. Then, with a staff committed to providing best-in-class service, we support you over the duration of the transaction.

Our Housing Credit Investments team is committed to making home a place of pride, power and belonging. That's why we reinvest every dollar of net income back into the industry.

We're here for the entire lifecycle of your investment. Our fully integrated Asset Management team handles everything from construction-monitoring, compliance obligations, to reviewing your capital account for tax issues. Above all, we ensure that your investment is optimized and sustainable for the long-term.

We take the time to understand your goals. That way, you can rely on us to provide an informed recommendation that meets your needs. Our experienced team of originators has deep knowledge of local markets. We work with sponsors every day across the country. And we've cultivated a network of relationships with funders, policy leaders, and partners to support you.

Decades of housing experience have taught us the value of creativity. To maximize your proceeds, we match your needs with the right financing and favorable terms. To amplify your return and your impact, we help structure the financing that works best for you. Partner with us to optimize your project’s capitalization, and we'll help assemble your financing on your schedule.

Our fully-integrated Asset Management team is dedicated to ensuring that your property is sustainable for the long-term. We closely track operating partnerships and work with you when changes occur after a deal closes. Over the duration of the project, we closely monitor your account. And we’re proactive at the time of disposition—so that you can continue your work of creating good homes people can afford.

In all, we’ve worked with more than 152 investors over our decades of experience. Join us to get the competitive returns you’re looking for while you make an investment that changes lives.

Enterprise pioneered Low-Income Housing Tax Credit investments from the start, helping craft the original Housing Credit legislation, and was the first to introduce the tiered fund yield structure in multi-investor funds.

| Multi-Investor (National) | Multi-Investor (Regional-California) | Single-Investor ("Proprietary") |

|---|---|---|

| For more information regarding our Multi-Fund Offerings please contact Danielle Hammann or Dan Cooper. | Customizable to your investment needs | |

In 2025 alone, we closed over $1.51 billion in new property investments into 27 different funds and completed more than 75 dispositions. Our portfolio ranks among the highest performing in the industry.

This $190 million impact investing fund, focused on improving and preserving the affordability of properties in high-opportunity neighborhoods while investing in properties developed by housing providers of color, is supported by blue-chip investors like Comerica.

“Comerica remains committed to empowering our communities and delivering opportunities to create positive change. Partnerships like the Equitable Upward Mobility Fund share in our goal of eliminating barriers and creating opportunities to enrich and improve lives in the communities we serve and provides a path for equal access for minorities and developers of color.”

– Beatrice Kelly, Comerica Bank Senior Vice President of Community Development Lending

Our investment helped transform a parking lot into 60 units of permanent supportive housing.

Meet Our Team