This piece is part of our series, Policy Actions for Racial Equity (PARE), which explores the many ways housing policies contribute to racial disparities in our country.

Earlier this year, the Biden-Harris administration announced a set of actions intended to address racial bias in the home appraisal process. The announcement followed a two-year effort led by the Interagency Task Force on Property Appraisal and Valuation Equity (PAVE), an inaugural task force comprised of 13 federal agencies and offices directed to evaluate the causes, extent, and consequences of appraisal bias, as well as establish recommendations to eliminate racial and ethnic bias from the home valuation process.

The PAVE task force found that the legacies of past racist housing policies, along with industry practices that reinforce negative perceptions of neighborhoods with high concentrations of Black, Indigenous, and other people of color contributed to the under-valuation of homes in majority-BIPOC neighborhoods and the loss of billions of dollars in wealth for their owners.

The Administration’s announcement follows the recommendations of the task force and includes bold steps to root out systemic sources of appraisal bias. Given the potential of these actions to dramatically change home valuation processes and wealth-building potential for BIPOC families, it is worth exploring further what appraisal bias is, how it affects households and neighborhoods, and how the Administration’s recent actions – along with others already underway at the federal, state, and local levels – could reverse its impacts.

Appraisals and Appraisal Bias

An appraisal is conducted by a professionally certified appraiser to provide a mortgage lender an objective estimate of a home's financial value based on several factors, including local market conditions, the physical state and aspects of the house, and sales data comparisons on recently sold neighboring homes. An appraisal is often conducted during the purchase or refinancing of a home, and it typically informs the maximum loan amount and potential resale value of the property. In addition to determining the value of a house, an appraisal also reflects the perceived value of a home’s neighborhood, as proximity to resources, schools, work opportunities, and leisure amenities also account for a home’s perceived value.

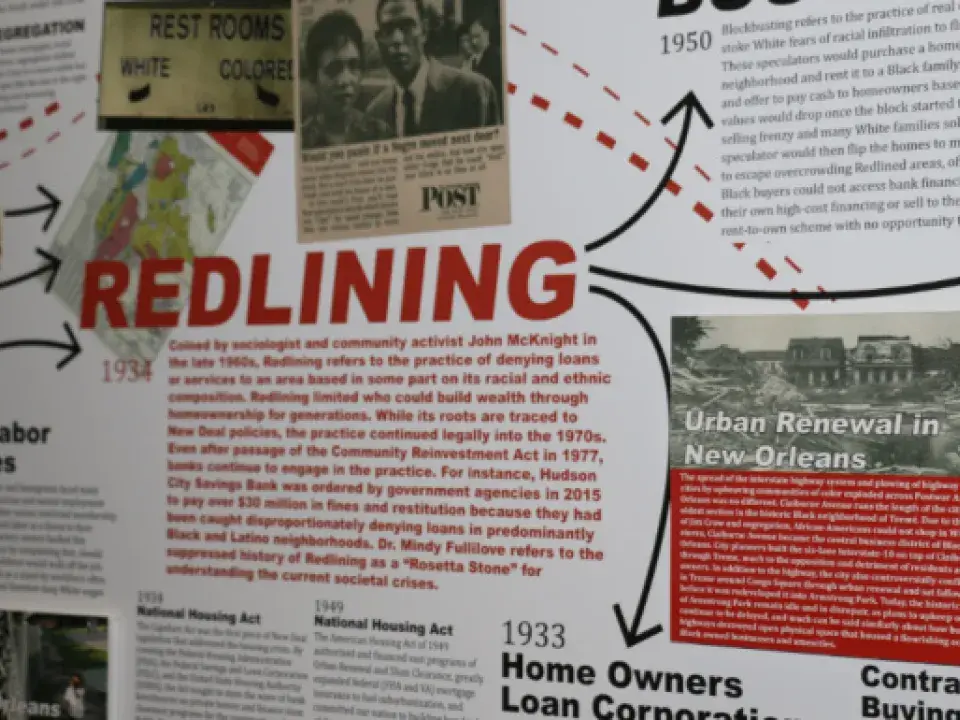

Bias in the appraisal process occurs when the race or ethnicity of a homeowner, or of the population in the surrounding area, influences the resulting valuation of a home. When racial discrimination in housing was legal, it was common – and sometimes required – to include race as a factor in determining home values. The same color-coded maps that mortgage lenders used to delineate certain neighborhoods as credit-worthy were also used by appraisers to determine the value of a property. While the Fair Housing Act, the Equal Credit Opportunity Act, and other civil rights legislation now prohibit the explicit use of race to determine the value of property, appraisal values are still rooted in prior home sale prices that were determined before these anti-discrimination laws were enacted. This practice exacerbates inequality by sustaining the price elevation of homes in predominantly white communities and preserving a standard of undervalued homes in communities of color.

Adding to the effect of past policies, multiple studies have shown that the modern-day appraisal process relies on a white-dominated racial hierarchy that assumes and discounts characteristics associated with majority-BIPOC neighborhoods, even when such characteristics may not exist or are similar to those in majority-white neighborhoods.

In their recent report, "Appraised: The Persistent Evaluation of White Neighborhoods as More Valuable Than Communities of Color,” Julia Howell and Elizabeth Korver-Glenn found an overall pattern of home appraisals in majority-white neighborhoods at double the value of appraisals in communities of color regardless of similarities in property and neighborhood characteristics. Their research also revealed that in 2021 the gap between appraisal values in majority-white neighborhoods and neighborhoods of color was $370,000, which is a figure that has drastically widened by 75% over the past decade.

As the availability of appraisal data expands and its granularity increases, housing policy practitioners and legislators have begun to grasp the extent to which appraisal bias impacts the expansion of the racial wealth gap by limiting the equity homeowners of color are able to gain. In recent years, research and news stories have also highlighted the pervasive nature of systemic racial bias in home valuations. For example, research from Andre Perry and Jonathan Rothwell at the Brookings Institute found that homes in majority-Black neighborhoods are almost twice as likely as those in majority-white neighborhoods to be under-appraised relative to their sales price and estimate the total effect of this undervaluation at $162 billion.

Actions to Combat Appraisal Bias

The Biden-Harris administration and state and local governments have started taking actions to address the harms of appraisal bias. In October 2022, the Federal Housing Finance Agency released the Uniform Appraisal Dataset (UAD) Aggregate Statistics, which is a database consisting of 46 million single-family home appraisals available at the census tract level. The UAD database was recently expanded with new statistics and property characteristics to provide greater access to public information and further deter appraisal bias.

While the database has enabled extensive research into appraisal outcomes, the biases discovered through this research have led to several actions, including public hearings of the Appraisal Subcommittee hosted by the Consumer Financial Protection Bureau to increase knowledge of appraisal bias impact, and a proposed rule from a group of federal agencies that intends to make home appraisals computed by algorithms, such as automated valuation models (AVMs), more accurate and fairer.

Local government leaders have also discovered the prevalence of appraisal bias and the need to understand its impacts at the local level. The Philadelphia City Council, for example, established the Philadelphia Home Appraisal Bias Task Force to develop local solutions to work in conjunction with recommendations from the PAVE task force at the national level. In Maryland, state Senators commissioned a report to analyze the impact of factors, such as appraisals, refinance rates, and housing values on BIPOC communities in the state. The entrenched appraisal bias in majority-BIPOC neighborhoods was one of several findings from the study, suggesting the need for a finance assistance program as a tactic to address Maryland’s racialized housing inequalities.

Policy and Programmatic Solutions

The preliminary measures executed on the federal, state, and local levels have helped amplify the need for additional policy and programmatic solutions to eliminate appraisal bias. Researchers, housing advocates, and members of the PAVE task force have recommended considerable actions to advance equity in the home appraisal process. A measure that has been elevated by the PAVE task force is the expansion of consumer education about appraisal bias and protections against it. The measure includes steps to improve the reconsideration of value process for consumers who experience a biased appraisal and a public awareness campaign to educate them about their rights.

Professional appraisal and real estate associations have also started exploring changes to increase access to and diversity in the appraisal profession as a method to expand equity. The Appraiser Qualifications Board (AQB), the national organization that sets professional standards for appraiser education and certification, has approved a computer program model to counter the challenges prospective appraisers face with completing the required 1,000+ service hour apprenticeship under the supervision of a licensed appraiser. The computer model, called Practical Applications of Real Estate Appraisal, provides a digital system that enables prospective appraisers to bypass the need to find a licensed appraiser to supervise their training, which is an obstacle for many and has limited diversity in the field. The AQB has also added a mandatory requirement for education on fair housing law that will be implemented in 2026. In addition to the actions of the AQB, the National Association of Real Estate Brokers will launch a partnership with HUD this month to host trainings and roundtables for housing counselors on strategies to address appraisal bias and discrimination in the housing market.

Researchers and federal agencies have also recommended the modernization of the current appraisal method. Howell and Korver-Glenn recommend an appraisal process that does not rely on past sales and decouples land value from the racial and socioeconomic attributes of homeowners. Other appraisal modernization solutions involve the continued use and improvement of technology-based valuation tools, such as AVMs. Continued momentum from the appraisal industry and the federal government is crucial to ensure that solutions are implemented to remove appraisal bias and create a more equitable environment for homeownership.

We encourage all who believe in the need to create a just society to read, discuss, and share the PARE blog series as we learn and act to address the impacts of housing policies on racial equity in America. We also invite you to join us in this conversation, by suggesting additional topics and sharing resources for how we can advocate for greater racial equity. If you’d like to offer feedback on our body of work, please reach out to the Public Policy team. You can also check out our blog and subscribe to our daily and bi-weekly policy newsletters for more information on Enterprise’s federal, state, and local policy advocacy and racial equity work.